Student Loan Default Rates Continue to Drop

For the third consecutive year, overall student loan cohort default rates (CDRs) have dropped, according to the Department of Education. The three-year CDR for FY 2012, based on borrowers who entered repayment in FY 2012 and defaulted by the end of FY 2014, dropped to 11.8 percent, compared to 13.7 percent and 14.7 percent for FYs 2011 and 2010 respectively.

The data also show the rates for each of the sectors have dropped as well, although the for-profit sector continues to have the highest rate of defaults:

- The FY 2012 rate for private 4-year schools dropped to 6.3 percent (FY 2011 - 7%; FY 2010 - 8%).

- The FY 2012 rate for public 4-year schools is 7.6 percent (FY 2011 - 8.9%; FY 2010 - 9.3%).

- The FY 2012 rate for proprietary schools is 14.7 percent (FY 2011 – 18.6 %; FY 2010 – 22.1%).

The Department also released the FY 2012 CDR data by state and institution type.

Schools are denied Title IV eligibility if they have a default rate of 30% for three consecutive years, or a 40% default rate for one year. Fifteen schools received consecutive years of high CDRs that could disqualify them from Title IV eligibility. According to Robert Kelchen, an assistant professor in the Department of Education Leadership, Management and Policy at Seton Hall University, 100 schools had rates over 30 percent for FY 2012, a worrisome indicator that more schools could lose Title IV eligibility in the future.

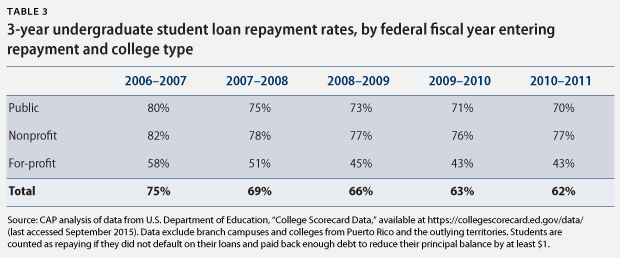

A mix of reasons has been offered to explain the rate decline: the improving economy; increased use of income-driven repayment plans; and borrowers being in forbearance or deferment status. Some of these reasons suggest that the cohort default rate does not provide a reliable reflection of borrowers’ difficulty repaying their loans. A repayment rate which captures struggling borrowers, as well as defaulters, may provide a more complete picture. Repayment rates are based on borrowers who have reduced loan principal by at least one dollar. Such a reduction might not take place during forbearance, deferment, or income-driven repayment. The Brookings Institution and the Center for American Progress estimate that only about two-thirds of borrowers are actually reducing their loan principal.

Based on the recently released College Scorecard, loan repayments rates have declined in recent years. So while actual defaults are going down, loan repayment rates are not improving.

{kind=link}

The total number of borrowers in default is estimated to be about 7 million. This figure has raised policy questions about the need to change bankruptcy restrictions on student loans and the possibility of requiring institutions to share in the cost of the defaults.

For more information, please contact:

Maureen Budetti