Student Loan Default Rates Continue Drop

The overall student loan cohort default rate (CDR) dropped this year by a half percent, according to the Department of Education. The three-year CDR for FY 2013, based on borrowers who entered repayment in FY 2013, and defaulted by the end of FY 2015, dropped to 11.3 percent, compared to 11.8 percent for 2012 and 14.7 percent for FYs 2011 and 2010 respectively.

The data also show the rates for the public and for-profit sectors have dropped as well, although the for-profit sector continues to have the highest rate of defaults:

- The FY 2013 overall rate for private 4-year schools is 6.5 percent, a slight increase from 6.3 percent in FY 2012, after several years of declining rates (FY 2012 – 6.3%; FY 2011 - 7%; FY 2010 - 8%).

- The FY 2013 rate for public 4-year schools is 7.3 percent (FY 2012 – 7.6%; FY 2011 - 8.9%; FY 2010 - 9.3%).

- The FY 2013 rate for the public 2-year institutions is 18.5%, down from 19.1% the previous year.

- The FY 2013 overall rate for proprietary schools is 15 percent (FY 2012 – 15.8%; FY 2011 – 19.1%; FY 2010 – 21.8%). (This is a decline of more than 5%, but is still the highest over-all sector.)

The decrease in the default rate does not necessarily mean that borrowers are no longer struggling with repayment. Loans in forbearance and deferment are not considered to be in default even though no repayment is being made. In addition, the several income-driven repayment (IDR) programs enable borrowers to reduce their level of payment based on their income, and thus avoid default. In some cases, a legitimately determined payment amount of “0” is considered acceptable, and the loan is not in default. According to the Department of Education, 4.6 million borrowers are enrolled in some form of IDR. This is an increase of 48 percent since December 2014, and 140 percent since December 2013.

Schools are denied Title IV eligibility if they have a default rate of 30 percent or more for three consecutive years, or a 40 percent default rate in one year. Ten schools were at a level that could disqualify them from Title IV eligibility; nine were for-profit schools and one was a tribal college.

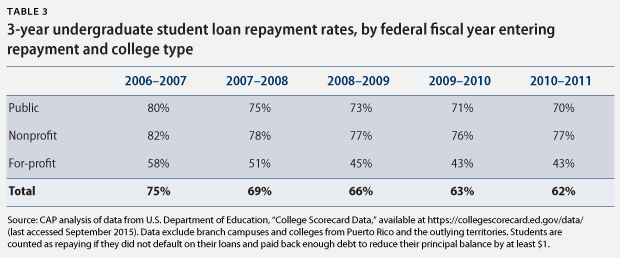

A mix of reasons has been offered to explain the decline in default rates: the improving economy; increased use of income-driven repayment plans; and borrowers being in forbearance or deferment status. Some of these reasons suggest that the cohort default rate does not provide a reliable reflection of borrowers’ difficulty repaying their loans. A repayment rate which captures struggling borrowers, as well as defaulters, may provide a more complete picture. Repayment rates are based on borrowers who have reduced loan principal by at least one dollar. Such a reduction might not take place during forbearance, deferment, or income-driven repayment. The Brookings Institution has estimated that about two-thirds of borrowers are actually reducing their loan principal. Based on information from the College Scorecard, loan repayment rates declined from 2006-2007 through 2010-2011. So while actual defaults are going down, loan repayment rates are not improving.

{kind=link}

The total number of borrowers who have not made a loan payment for at least 9 months (e.g., the total number of borrowers who are delinquent and those who have defaulted), is 8.1 million. This figure has raised policy questions about the need to change bankruptcy restrictions on student loans and the possibility of requiring institutions to share in the cost of the defaults.

For more information, please contact:

Maureen Budetti